Why I'm Still Bullish on Ethereum (And Why It Matters for Your Clients)

By Lucas Campbell, Elkhorn Research — June 2026

Ethereum has been essentially flat for five years.

While Bitcoin hit new all-time highs and the S&P kept climbing, ETH has ranged between roughly $2,000 and $4,000 — barely breaking $5,000 at the top of this cycle. For advisors who fielded client questions about ETH a few years ago, that's a hard track record to explain.

But price stagnation and deteriorating fundamentals are different things. In Ethereum's case, they're telling very different stories right now.

This piece lays out why I'm still constructive on ETH, what's actually happening on the network, and why the most important chapter of this asset's story may still be ahead — particularly for the clients you serve.

The Price Picture

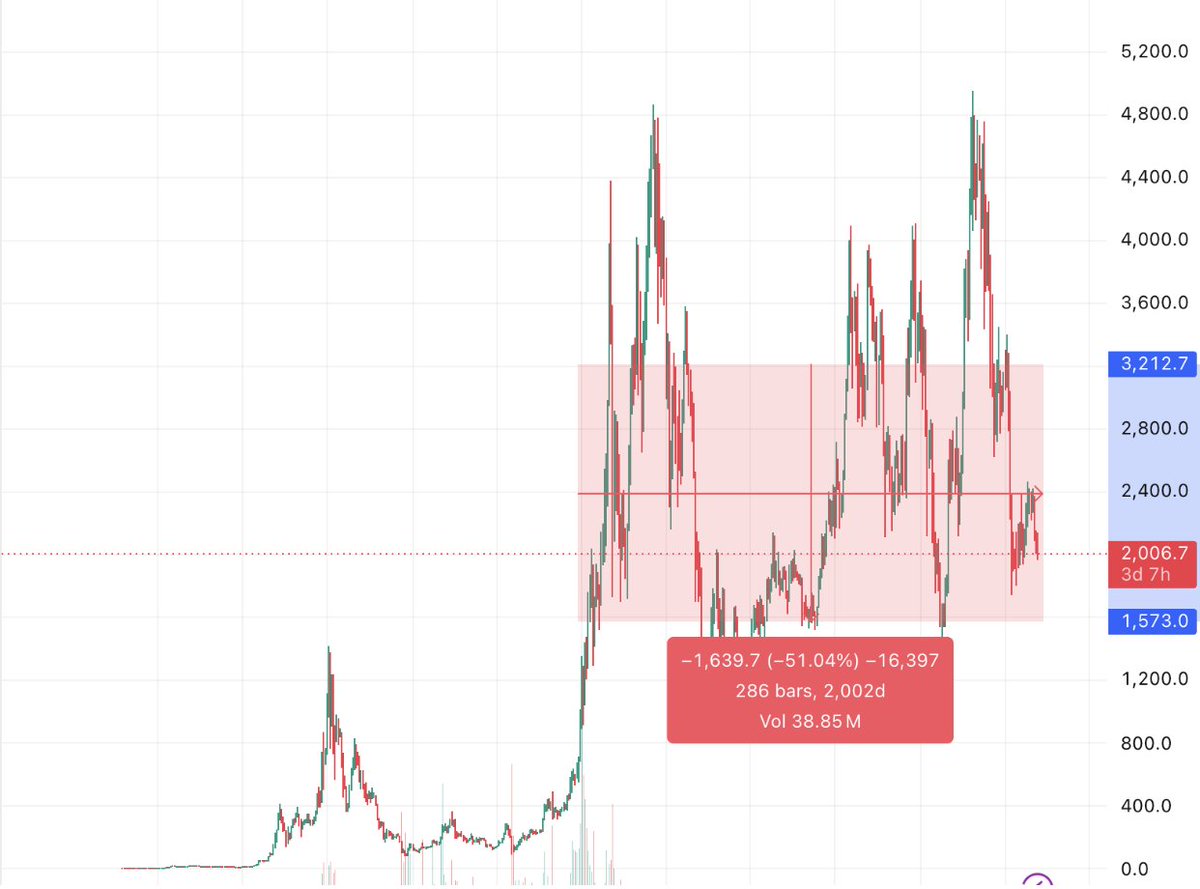

ETH is sitting roughly 60% below last cycle's all-time high. Anyone holding it over the past five years has largely been flat while nearly every other asset class has moved higher.

When you look at the actual chart rather than the narrative around it, what you see is a five-year consolidation — not a collapse. Ethereum still commands a $250 billion market cap, putting it in the top 100 assets globally. It's oscillating in a range.

That pattern — extended consolidation after a fast initial run — shows up repeatedly in the history of transformative assets. Three examples your clients will recognize:

Amazon went through a 3,948-day consolidation, trading in a narrow range for over a decade after its initial run. It then became one of the most valuable companies in the world.

NVIDIA spent 2,814 days in a tight range after its initial rise. It's now the most valuable semiconductor company on the planet.

Microsoft went through a 5,023-day consolidation after the dot-com peak. If you bought MSFT in 2000, you didn't break even until 2014. It's now one of the best-performing large-cap stocks of the past decade.

Apple spent 6,147 days in a range before its breakout. It's now the most valuable company in the world.

None of these examples guarantee anything about ETH's trajectory. But they establish that flat price action after a fast run-up is a recognizable historical pattern — and that writing off an asset during its consolidation has historically been expensive.

What's Actually Happening on the Network

The more important question is whether the underlying network is healthy or in decline. Here the data is unambiguous.

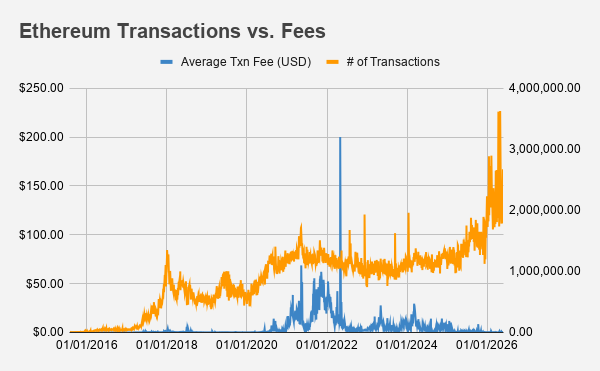

Ethereum is processing an average of 2.27 million transactions per day. Average fees have dropped to $0.27 — down from $50–$100+ during the 2021 peak. More throughput, lower cost, simultaneously.

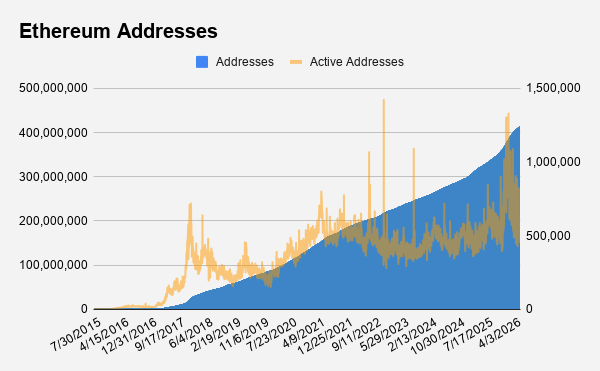

The network now has over 400 million total addresses, growing at roughly 0.08% per day through 2026. Active addresses recently crossed 1 million in a single day.

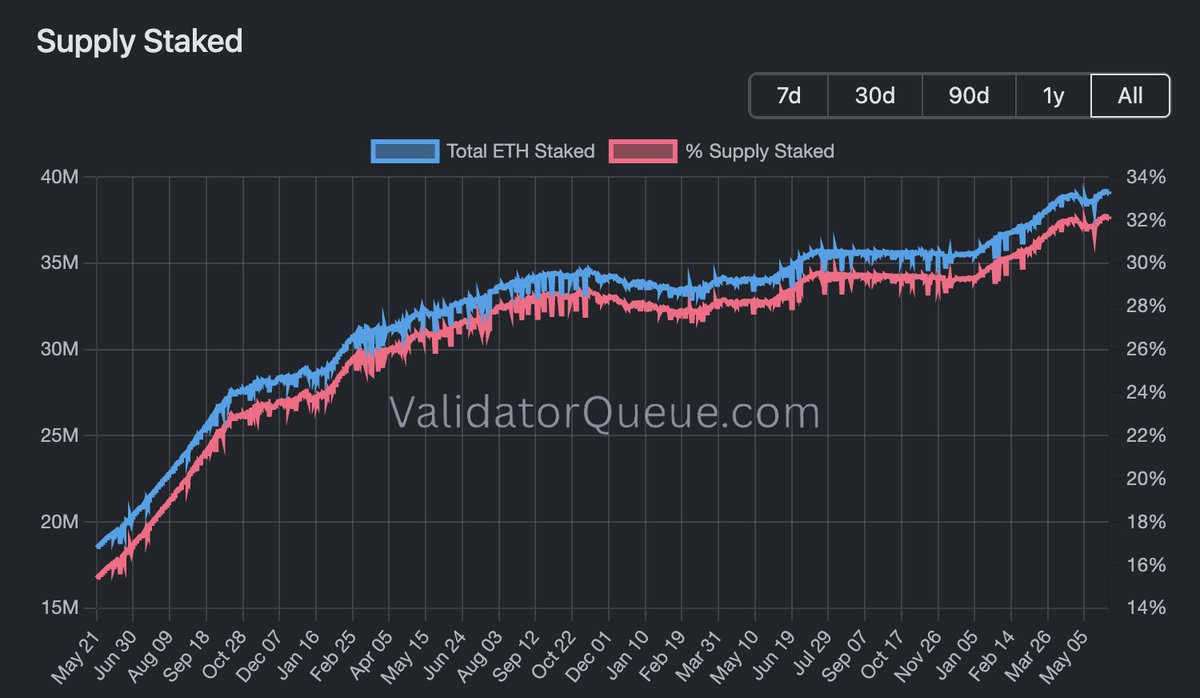

And increasingly, participants aren't just using the network — they're locking capital into it. Over 39 million ETH are now staked, representing roughly 32% of the total supply. Validators are growing, and the network is becoming more secure as a result.

This is the opposite of what you'd expect from a network people have abandoned.

The Thesis

My thesis on Ethereum has been consistent since I joined the space: all value will eventually be tokenized, and Ethereum is the settlement layer for tokenized value.

For the first decade, Ethereum was primarily the home of crypto-native experimentation — decentralized finance, NFTs, speculative protocols. That chapter produced real innovation, but it looked to most of traditional finance like a solution in search of a problem.

The next chapter is different. It's about traditional financial assets coming onchain. And that's a story your clients have a direct stake in.

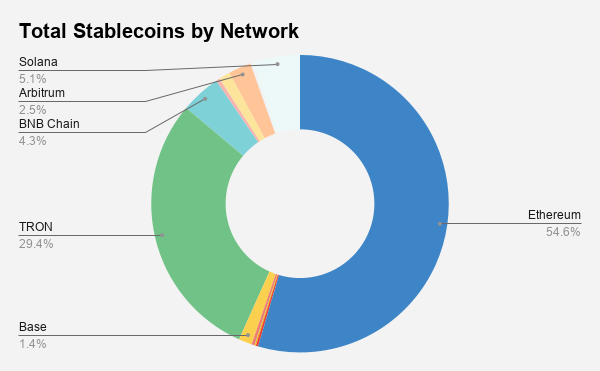

Stablecoins were the first proof point. The market grew to over $330 billion in circulating supply. Ethereum captures 54.6% of total stablecoin market share — about $180 billion sitting on Ethereum's infrastructure right now. That's not because Ethereum was the only option. It's because institutions kept choosing it.

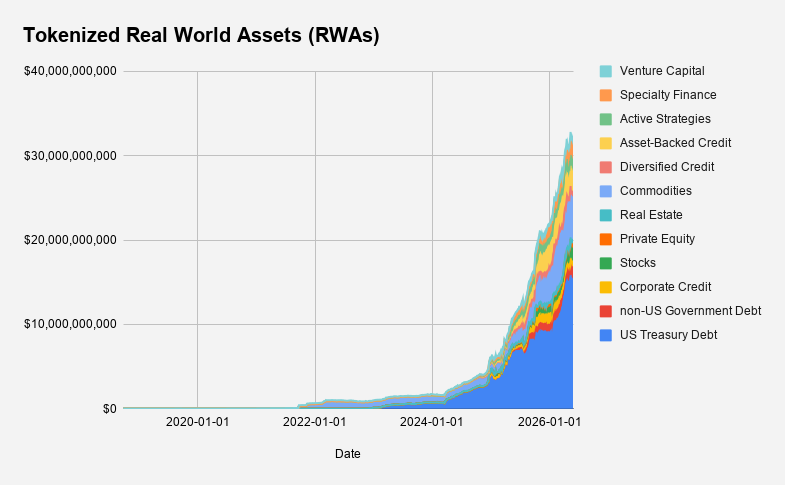

Real World Assets are the current wave. Tokenized Treasuries, equities, funds, private credit — traditional financial assets moving onchain. Total value of tokenized RWAs has surpassed $30 billion and the growth curve is steep.

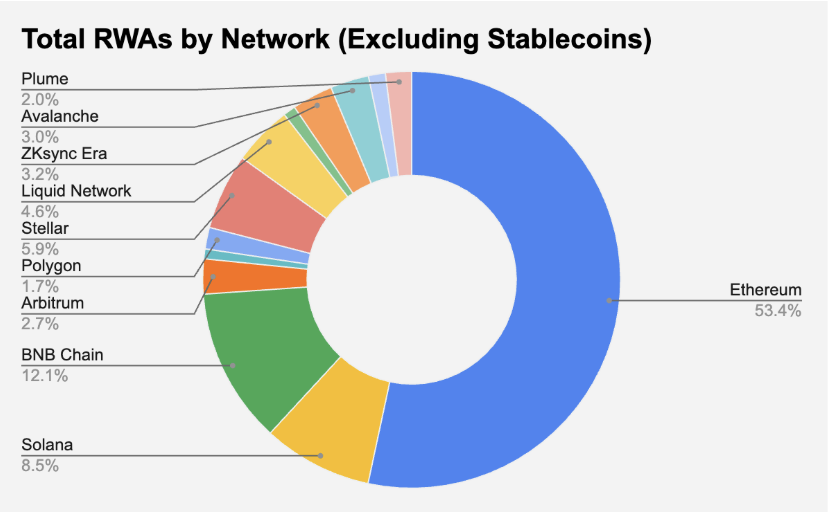

Ethereum's market share here mirrors stablecoins: 53.4% of all RWAs live on Ethereum — more than four times its nearest competitor.

The reason is the same as stablecoins: reliability. Ten-plus years of continuous uptime. No successful network-level attacks. A globally distributed validator set that no single party controls. When a bank, asset manager, or clearing house decides to put customer assets on a blockchain, they're making a decision they can't easily unwind. Ethereum is the only smart contract platform that can credibly make the case for that level of trust today.

The names choosing Ethereum aren't small players.

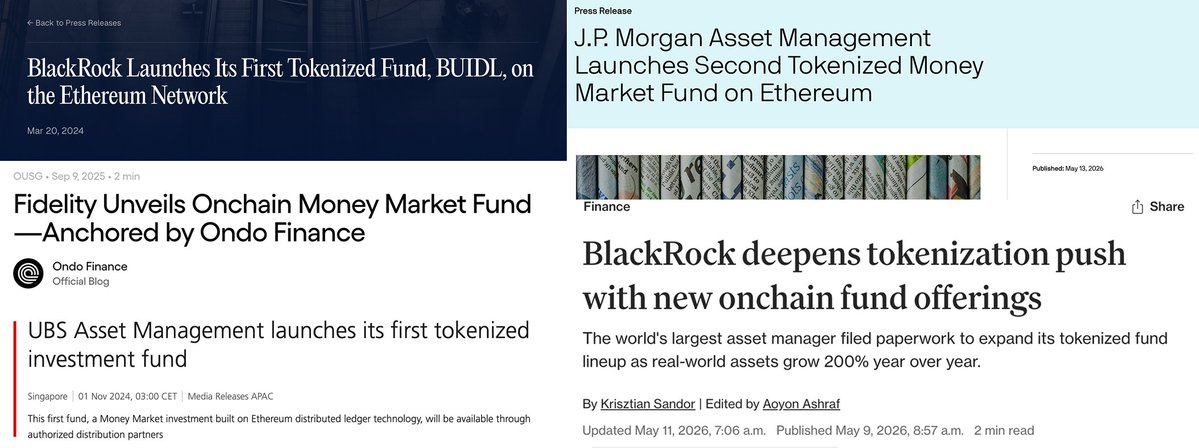

BlackRock launched its first tokenized fund (BUIDL) on Ethereum in March 2024. J.P. Morgan Asset Management followed with a second tokenized money market fund on Ethereum. Fidelity unveiled an onchain money market fund anchored by Ondo Finance. UBS Asset Management launched its first tokenized investment fund. These aren't experiments. They're product launches from institutions that have spent years evaluating their options.

The regulatory environment is moving in the same direction. The GENIUS Act made stablecoins a regulated asset class. The CLARITY Act — which prediction markets currently put at roughly 55% probability of passing in 2026 — would provide the broader framework for tokenizing traditional financial instruments.

Traditional financial assets are moving onchain. The question is which network captures the institutional trust for that transition. The early data is consistent.

The Bear Case

The honest bear case is that Ethereum won't capture enough of this to matter for the price. Faster competitors may close the reliability gap as they mature. Fee revenue from tokenization activity may accrue to Layer 2 networks rather than Ethereum's base layer, diluting ETH's value capture even if the thesis plays out.

These are real risks worth tracking. The current data says Ethereum is winning — but early leads in technology transitions have disappeared before.

What This Means for Your Practice

The client conversation around Ethereum is worth having with care. The five-year price picture is real and shouldn't be dismissed. But the network — growing throughput, falling costs, 39M ETH staked, $180B in stablecoins and $30B in tokenized assets living on its infrastructure — is telling a different story than the price alone.

That distinction matters when clients ask whether the Ethereum story is over. It's not a story about price recovery. It's a story about whether the network that spent its first decade proving itself is now becoming the infrastructure layer for a meaningful portion of global finance.

That's a question worth having an informed answer to.

Lucas Campbell is the founder of Elkhorn Research and former Editor in Chief at a leading crypto media and education platform. He has advised on $10B+ in digital asset launches, including Optimism, Eigenlayer, and ENS.

Research and education only. Nothing here constitutes investment advice or a recommendation to buy or sell any security or digital asset.